December 2019 Real Estate News & Updates

Please let me know if you would like to receive my monthly newsletter by messaging me your email address. I promise this will be the only thing I will email you and I will not share your email address.

Thank you,

Kate Spadarotto

The Current 5 Most Popular Real Estate Questions and Answers

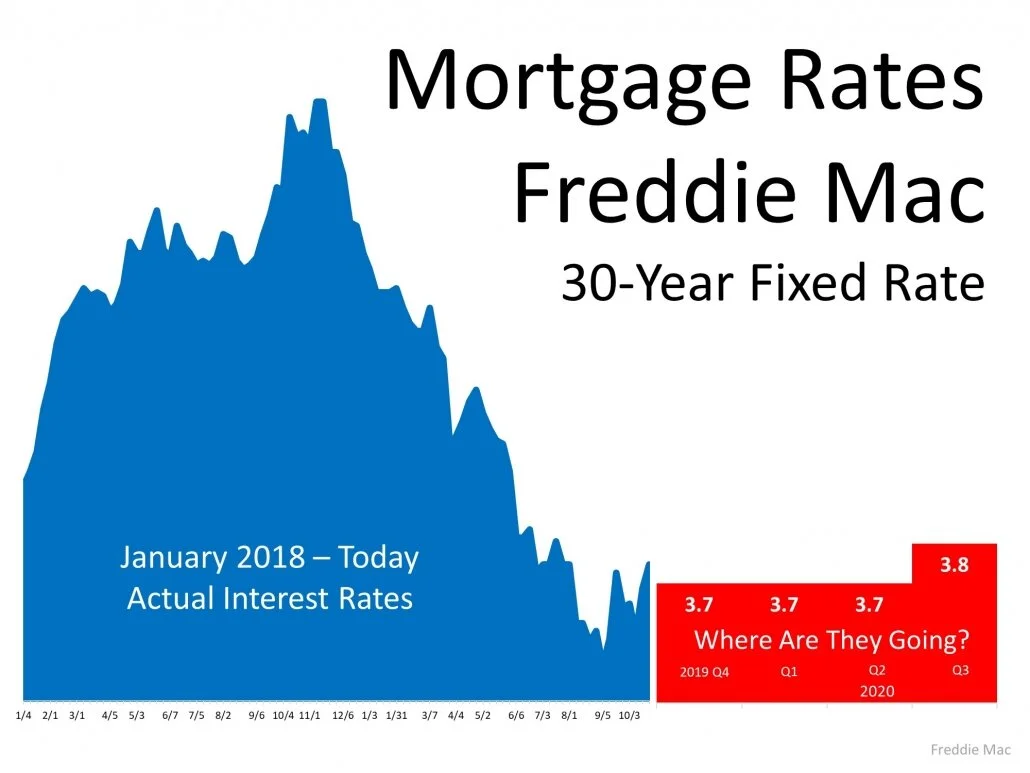

Are Mortgage Rates Going to Go Up?

With the price of homes going up due to a strong economy and high demand, mortgage rates are helping to balance it all out by keeping things affordable.

Essentially, the lower your mortgage rate, the lower your monthly payments.

With Freddie Mac predicting that mortgage rates should stay where they are for the next 12 months, this shouldn’t be changing anytime soon.

2. Is Now a Good Time to Buy or Sell?

The short answer is: yes and yes.

As said above, low mortgage rates mean it’s a great time for anyone to buy: whether it’s for the first, second or fifth time. This is especially true for someone looking to upgrade their home and purchase one in a higher bracket.

The low mortgage rate will help you afford more house at a lower monthly payment.

Combine that with low inventory and high demand, and you have an equally good seller’s market. This goes especially for homes in the low to mid-range.

3. Are Home Prices Going to Keep Rising?

Data from the leading experts in real estate and mortgage lending says yes.

But before anyone panics, that means now is the best time to buy and sell.

With mortgage rates expecting to stay where they are and an anticipated 3.5-5% price appreciation happening in the next year, this is without a doubt the best time to buy.

Waiting only means one thing: spending more for the same house.

Take a look at our price appreciation slide so you can show them the facts to back it up.

4. Do I Need to Update My Home Before I Sell It?

Making updates could mean a higher asking price. It could also mean investment loss.

Depending on the type of updates needed, the market’s current low inventory levels put any home that hits the market in a good position to sell. Yes, some homeowners prefer to buy a “turn-key” home. On the flip side, others may want to make the updates themselves, so everything is to their taste.

Check out this post on which updates have the highest return on investment.

5. Is a Recession Going to Cause Home Prices to Fall?

Yes, it’s very likely a recession will hit either next year or the year after. However, this in no way means a housing market catastrophe like the one that occurred in 2008.

Here’s why:

-Of the last five recessions, only two saw a decline in home values with three seeing increases.

-The two that saw declines were in 1991 (-1.9%) and of course, 2008 (-19.7%).

-The current market does not remotely resemble the one before the 2008 crash.

-The top causes for the next recession have nothing to do with the housing market, unlike that of 2008 when risky borrowing led to a bubble that was bound to burst.

6 Graphs Showing the Strength of the Current Housing Market

Some Highlights:

Keeping an eye on the current status of the housing market is one of the best ways to make powerful and confident decisions when buying or selling a home.

Mortgage rates remaining near historic lows and houses selling in an average of only 29 days are just two key elements driving the strength of today’s market.

With the national data shown here, make sure to also determine what’s happening in your local market so you are fully informed when you’re ready to make your next move.

Top 10 Most Expensive Cities in the U.S.

People relocating for business, new jobs or simply planning a vacation can benefit from knowing details about the most expensive cities in the United States. Understanding how much it costs to live in a city, and why, can make or break a decision to move. Not surprisingly, California cities dominate the list of America’s priciest cities.

KEY TAKEAWAYS

Cities offer a variety of employment opportunities along with loads of culture, sports, dining, and entertainment.

Because of the desire to live in cities, they can become quite expensive places to live.

In the U.S., New York City is the most pricey to live in, followed by San Francisco - however, NYC is only #9 on the world's most expensive cities.

Fast Fact: The most expensive cities to live in 2019 in the world are Hong Kong, Tokyo, and Singapore. New York City, the only American city to make the top 10, comes in at #9.

1. New York City, New York

New York City leads the pack as the most expensive city in the United States; the city, with a population exceeding 8.3 million, also tops lists of the world’s most expensive cities. The cost of living in New York is a whopping 120% higher than the national average. The average cost of homes in New York is about $501,000, compared to the national average price, which hovers around $181,000; home prices range across the five boroughs, with home prices in Manhattan exceeding $1 million. Everything costs more in New York City, from groceries to public transportation. At approximately 4.1%, as of May 2019, the city’s unemployment rate is lower than the national average of 4.3%, further encouraging people the world over to pin their hopes and dreams on making it in New York.

2. San Francisco, California

People make the decision to leave San Francisco every day, as the city’s staggeringly high cost of living and out-of-reach housing prices have been known to break many a bank. Homes cost an average of $820,000 inside the city, whose major industries include tourism, IT and financial services. It takes more than $119,000 to live well in San Francisco, but unemployment remains extremely low at just 1.9%, as of May 2019, due to highly favorable conditions offered to entrepreneurs and the one-third of all U.S. venture capital that these up-and-coming businesses attract.

3. Honolulu, Hawaii

Honolulu residents pay a lot of money for just about everything. Groceries alone cost 55% more than anywhere else in the United States; utilities cost 71% more than the national average. At $58,397, the average household income does not far exceed the average income of other expensive cities in the country. However, people in Honolulu can expect to pay 87% more than the average American pays for one dozen eggs. Honolulu enjoys an exceptionally low unemployment rate of 2.8%, as of May 2019, which means that, if nothing else, people with jobs on this Pacific island paradise can afford to eat omelets.

4. Boston, Massachusetts

Groceries and health care cost a lot of money in Boston, exceeding the average national cost by more than 20%. The city enjoys a robust higher education environment, a booming tech scene that rivals Silicon Valley and historic sites dating back to the 13 original colonies, which makes it one of the nation’s leading tourist destinations. All of these add up to an unemployment rate of 3.6%, but city residents fork out big money to live in Boston; the average home value hovers around $374,000, the median household income averages about $53,163, and it takes approximately $84,000 to live well.

5. Washington, D.C.

Being the seat of the world’s most powerful nation accounts for Washington, D.C.’s high cost of living. Government and private-sector jobs abound in the city, thanks to numerous federal agencies, think tanks, lobbying firms and a robust tourism sector. Average home values in the District stand at approximately $443,000, and the average household income is about $64,267. Similar to Boston, it takes about $83,000 to live well in Washington, D.C.

6. Oakland, California

Being located on the opposite end of the Bay Bridge might make living in Oakland a cheaper alternative to San Francisco, but the city is still a more expensive place to live than most cities in the United States. For $1,673 per month, renting an apartment in Oakland costs double the price of renting in other U.S. cities; the average home value runs about $449,800.

7. San Jose, California

Anyone looking to escape high prices in the Bay Area can head south to San Jose, located within commuting distance of San Francisco and Oakland. The presence of Silicon Valley makes everything in San Jose expensive, including housing that averages about $575,000. The median household income hovers around $81,000. The numerous tech industry employers in the city account for a well lower-than-average unemployment rate of 2.4%, as of May 2019.

8. San Diego, California

A strong defense department presence and military contracting firms, such as Northrop Grumman Corporation (NYSE: NOC) and Science Applications International Corporation (NYSE: SAIC), make California’s southernmost city one of the priciest in America. The cost of living in this city of approximately 1.3 million is 30% higher than the average cost of living in the United States. San Diego’s median household income hovers around $63,990, meaning that many residents can enjoy luxuries such as high-end eateries, yacht clubs and other pricey forms of entertainment. The average home value stands at approximately $477,800. San Diego’s unemployment rate of 3.8% edges close to the national average.

9. Los Angeles, California

Los Angeles brings to mind wealthy, glamorous movie stars, but the movie industry plays a small role in the city’s booming economy. The city's shipping industry also plays a role, as the Port of Los Angeles is one of the busiest ports in the world. A bustling manufacturing sector and a noteworthy start-up scene contribute to the city’s high cost of living. Certain ZIP codes, such as the much-ballyhooed 90210, drive up housing costs; the average home value in Los Angeles is $470,000. The median household income is around $49,745. It takes approximately $74,371 per year to live well in Los Angeles, and more than 20% of the city’s residents live in poverty.

10. Miami, Florida

Miami is the only southern U.S. city ranking on the top 10 most expensive list. A high population of wealthy foreigners, the presence of numerous international financial institutions and the busiest cruise ship port in the world give life in Miami a high price tag. The city’s average household income stands at about $48,100, and the unemployment rate of about 4.4% is just a hair above the national average. It takes about $77,000 to live well in this stylish city replete with newly constructed residential and commercial buildings.

Experts Predict a Strong Housing Market for the Rest of 2019

We’re in the back half of the year, and with a decline in interest rates as well as home price and wage appreciation, many are wondering what the predictions are for the remainder of 2019.

Here’s what some of the experts have to say:

Ralph McLaughlin, Deputy Chief Economist for CoreLogic

“We see the cooldown flattening or even reversing course in the coming months and expect the housing market to continue coming into balance. In the meantime, buyers are likely claiming some ground from what has been seller’s territory over the past few years. If mortgage rates stay low, wages continue to grow, and inventory picks up, we can expect the U.S. housing market to further stabilize throughout the remainder of the year.”

Lawrence Yun, Chief Economist at NAR

“We expect the second half of year will be notably better than the first half in terms of home sales, mainly because of lower mortgage rates.”

“The drop in mortgage rates continues to stimulate the real estate market and the economy. Home purchase demand is up five percent from a year ago and has noticeably strengthened since the early summer months…The benefit of lower mortgage rates is not only shoring up home sales, but also providing support to homeowner balance sheets via higher monthly cash flow and steadily rising home equity.”

Bottom Line

The housing market will be strong for the rest of 2019. If you’d like to know more about your specific market, contact a local real estate professional to find out what’s happening in your area.

National Senior Citizens Day: Seniors are on the Move in the Real Estate Market

Did you know August 21st is National Senior Citizens Day? According to the United States Census, we honor senior citizens today because,

“Throughout our history, older people have achieved much for our families, our communities, and our country. That remains true today and gives us ample reason…to reserve a special day in honor of the senior citizens who mean so much to our land.”

To give proper recognition, we’re going to look at some senior-related data in the housing industry.

According to the Population Reference Bureau,

“The number of Americans ages 65 and older is projected to nearly double from 52 million in 2018 to 95 million by 2060, and the 65-and-older age group’s share of the total population will rise from 16 percent to 23 percent.”

Seniors Believe in Homeownership

In a recent report, Freddie Mac compared the homeownership rates of two groups of seniors: the Good Times Cohort (born from 1931-1941) and the Previous Generations (born in the 1930s). The data shows an increase in the homeownership rate for the Good Times Cohort because seniors are now aging in place, living longer, and maintaining a high quality of life into their later years.

This, however, does not mean all seniors are staying in place. Some are actively buying and selling homes. In the 2019 Home Buyers and Sellers Generational Trends Report, the National Association of Realtors® (NAR) showed the percentage of seniors buying and selling:

Here are some highlights from NAR’s report:

Buyers ages 54 to 63 had higher median household incomes and were more likely to be married couples.

12% of buyers ages 54 to 63 are first-time homebuyers, 5% (64 to 72), and 4% (73 to 93).

Buyers ages 54 to 63 purchased because of an interest in being closer to friends and families, job relocation, and the desire to own a home of their own.

Sellers 54 years and older often downsized and purchased a smaller, less expensive home than the one they sold.

Sellers ages 64 to 72 lived in their homes for 21 years or more.

Bottom Line

According to NAR’s report, 58% of buyers ages 64 to 72 said they need help from an agent to find the right home. The transition from a current home to a new one is significant to undertake, especially for anyone who has lived in the same house for many years. If you’re a senior thinking about the process, work with a local real estate professional who can help you make the move as smoothly as possible.

Do I Need a Permit for That? - Don't jeopardize a future sale.

When undertaking a remodel or home improvement project, how do you know when you need a building permit from your city government?

Cities require permits to ensure that the changes on a home go on record. The changes also are reviewed by an inspector to ensure they’re up to code. For example, if you decide to rewire your electricity panel , exposed wires could represent a safety issue to you and your home.

When homeowners sell their home, buyers and lenders will want to know if any remodels they did complied with building codes. So the permit could salvage a sale too.

“The general rule of thumb is that structural, electrical, plumbing, or mechanical work will require a permit,” notes Redfin at a recent blog post.

A fence installation or repair, window installations, plumbing and electrical work, replacing the water heater or changes to the ventilation system, as well as gas and wood fireplaces all will likely require a permit for the work. Also, any additions or upgrades made to the home, typically of $5,000 or more, will likely require a permit.

On the flip side, permits likely won’t be needed for painting, installing floors or faucets, or landscaping work.

Permit requirements vary by city. Check with the local building department to be on the safe side.

Source: https://www.redfin.com/blog/which-home-improvement-projects-require-a-permit/

Americans Have Never Felt This Good About Real Estate

Fannie Mae’s Home Purchase Sentiment Index surged to a new high as consumers became more upbeat about buying and selling, mortgage rates, and their jobs. Five of the six components measured by the index rose month over month.

“Consumer job confidence and favorable mortgage rate expectations lifted the HPSI to a new survey high in July, despite ongoing housing supply and affordability challenges,” says Doug Duncan, Fannie Mae’s senior vice president and chief economist. “Consumers appear to have shaken off a winter slump in sentiment amid strong income gains. Therefore, sentiment is positioned to take advantage of any supply that comes to market, particularly in the affordable category. However, recent financial market events following when the survey data were collected could weigh on consumer views looking ahead.”

Overall, the HPSI, based on a survey of 1,000 Americans, rose 7.2 points compared to a year ago to a record-high reading of 93.7 in July. Here are some highlights from the index’s latest readings:

Buying: The net share of Americans who said now is a good time to buy a home rose 3 percentage points from June to 26%, up 2 percentage points from a year ago.

Selling: The net share of consumers who say it’s a good time to sell rose 1 percentage point to 44%, up 3 percentage points from a year ago.

Home prices: The share of Americans who say home prices will go up over the next 12 months fell 1 percentage point to 37%, down 2 percentage points from a year ago.

Mortgage rates: The share of consumers who believe mortgage rates will drop over the next year rose 1 percentage point and is up 24 percentage points from a year ago.

Job stability: Americans are more confident about their job situation, with the share who say they’re not concerned about losing their job over the next year rising 8 percentage points to 81%. This is up 16 percentage points from a year ago.

Household incomes: The share of Americans who say their household income is significantly higher than 12 months ago rose by 1 percentage point to 21%, essentially unchanged from a year ago.

Source: “Home Purchase Sentiment Index,” Fannie Mae (Aug. 7, 2019)

Bottom Line

Consumers are feeling good about the real estate market. Since Americans are not worried about their jobs, see mortgage rates near an all-time low, and believe it is a good time to buy, the housing market will remain strong for the rest of the year.

Rising Affordability in Purchasing Real Estate

BY: JANN SWANSON

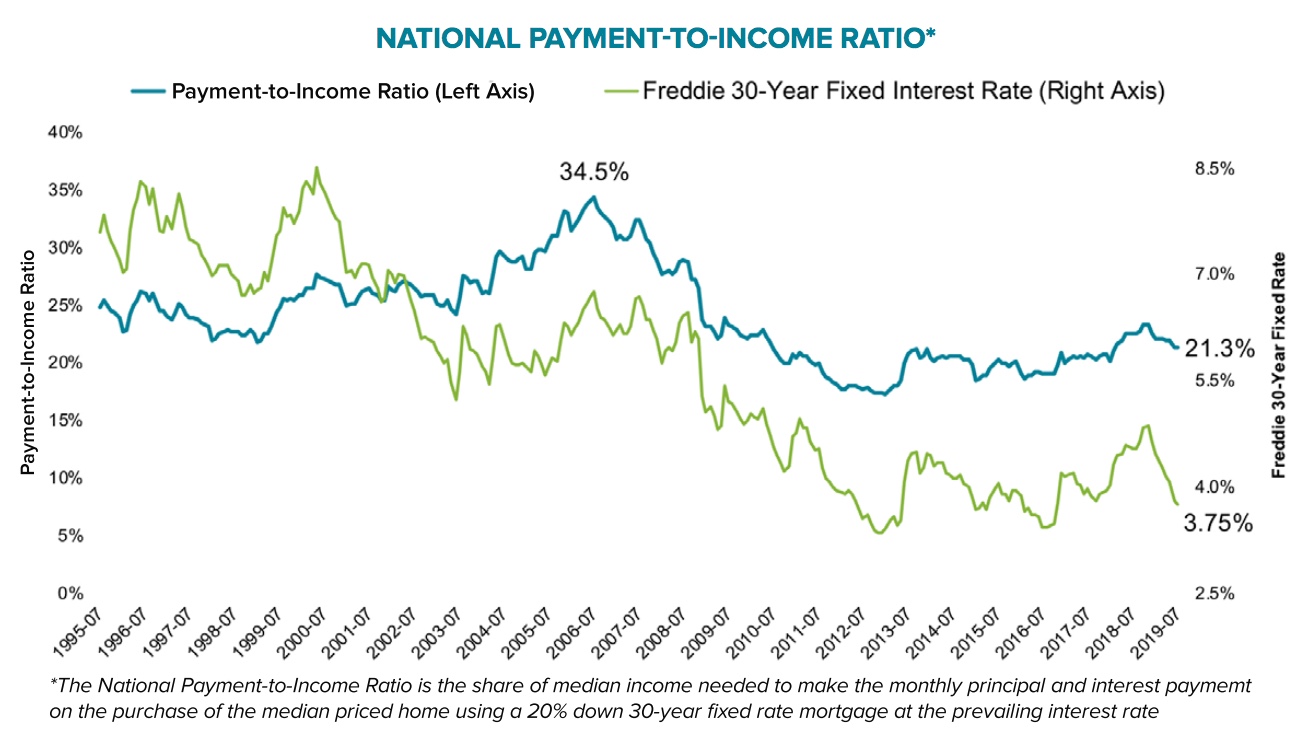

Black Knight has good news for potential homebuyers, especially those in the market for their first home. The new edition of the company's Mortgage Monitor says the recent decline in mortgage interest rates has made home affordability the best it has been in 18 months.

With the 30-year fixed-rate mortgage hovering around 3.75 percent, it now takes 21.3 percent of the nation's median monthly income to make a mortgage payment on the median priced home. This is down from 23.3 percent in November of last year and more affordable than the long-term ratio of around 25 percent that was in-play during a time when the market was generally considered to be "normal," 1995 to 2003. It is also much lower than the 34.5 percent ratio at the height of the housing boom.

The rising payment-to-income ratio, as it hit its recent peak last November, appeared to trigger a strong reaction in both sales and home prices. Given its relatively modest historical position, Black Knight suggests there may be heightened sensitivity to affordability concerns in today's market. Both existing and new home sales have been ragged since then and, although home prices continued to rise, that rate at which they did so slowed considerably.

The average home price has gone up by more than $12 thousand since interest rates peaked last November, but the monthly payment has declined by $108 for an average home purchased with a 20 percent down payment. Black Knight says this is the equivalent of a 15 percent increase in buying power and means a homebuyer could pay $45,000 more for a home without seeing an increase in the monthly payment.

Of course, with lower rates and higher affordability, demand is growing again. The company notes that, the 15-month pattern of price deceleration it had been tracking seems to have leveled off. The annual home price appreciation rate held steady in June at 3.78 percent.

Black Knight cautions that it takes time for impacts for interest rate changes to show up in housing market numbers; even after homebuyers react, there is a time lag due to contract, offer, closing, and recording times. Therefore, the flat appreciation rate from May to June could be just the beginning and the 3.75 interest rate that hit at the end of June may not show up in home sale and price changes until August or September.

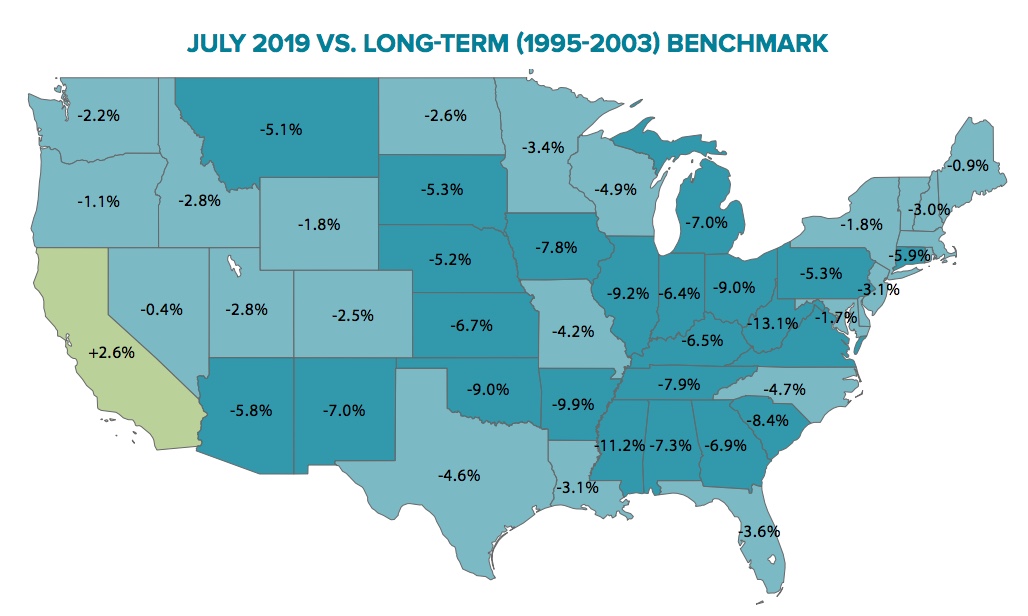

There is a large spread of payment to income ratios across the states, but affordability is improving. Where nine states were less affordable than their long-term norms back in November, only California and Hawaii remained so as of July.

Housing is least affordable along the western U.S. and parts of the northeast, while the Midwest and parts of the South are home to some of the lowest payment-to-income ratios. Not only is housing in the Midwest the most affordable, but it is also the furthest below its own long-term average, as income growth there has been more in line with home price growth than in other areas.

Even in California, however, affordability has improved. The state went from having one of the top five home price growth rates of any state (8.6 percent) one year ago to second-to-last as of June 2019, with home price growth slowing to just 1.3 percent year-over-year. The payment ratio in the state is now 34 percent, down 4 percentage point from November. That is, however, 2.5 points above its long-term ratio. Growth declines in several of the West Coast's largest markets has been significant up; prices in the last 12 months have increased by 1.1 percent or less in Los Angeles, San Francisco, San Diego and Seattle.

Price growth among condominiums have been experiencing greater slowing over the last 12 months than have prices of single-family homes. Up until then the two sets of prices had been rising in lockstep, but now condos are appreciating at 2.2 percent compared to single-family homes at 3.9 percent. That is a 40 percent differential. The company points out that condo prices are historically more volatile, they had a faster appreciation rate in the late 1990s and early 2000s, experienced a sharper downturn during the financial crisis and then recovered faster in 2012 to 2014. Now the tide may be turning again. The company said this could be due to a number of factors and it worth keeping an eye on.

Black Knight also provided an update on the prepayment rate which had been seeing some dramatic increases as rates declined. That, however, ended in June as activity fell by 7.5 percent. It was the first monthly decline since January and the company calls it surprising "given that refinance incentive continues to rise, and home sale driven prepayments typically increase from May to June."

The declines were evident across servicing portfolios, investor classes, interest type and vintages but the strongest reductions were among portfolio held loans, high credit score mortgages and loans originated last year. Those were the cohorts that had seen the largest increase in prepayments previous to June. Black Knight says the pullback may be due to sluggish refi-driven prepayments in June rather than (or potentially in combination with) lackluster home sale driven prepays

Millionaire to Millennials: The Costly Mistake of Not Buying Now

On his personal website, self-made millionaire David Bach makes a striking statement:

“Not prioritizing homeownership is the single biggest mistake millennials are making.”

He further stated, “Buying a home is an escalator to wealth.”

Bach explains:

“Young adults in particular aren’t hopping on this escalator, and it’s a costly mistake…If millennials don’t buy a home, their chances of actually having any wealth in this country are little to none.”

He then elaborates on the game of homeownership:

“Start by crunching the numbers…actually do the math...This way, you’re really clear on your goals and you won’t just say to yourself, ‘I’ll never afford this!'

A good rule of thumb is to make sure your total monthly housing payment doesn’t consume more than 30 percent of your take-home pay.”

Bach concludes by saying,

“Oftentimes, buying your first home means you’re not buying your dream home…You’re just getting into the market.”

Bottom Line

Whenever a well-respected millionaire gives investment advice, listeners usually clamor to hear it. This millionaire shares some simple and straightforward insights: “The fact is, you aren’t really in the game of building wealth until you own some real estate.”

Who is David Bach?

Bach is a self-made millionaire who has written nine consecutive New York Times bestsellers. His book, “The Automatic Millionaire,” spent 31 weeks on the New York Times bestseller list. He is one of the only business authors in history to have four books simultaneously on the New York Times, Wall Street Journal, BusinessWeek, and USA Today bestseller lists.

He has been a contributor to NBC’s Today Show, appearing more than 100 times, as well as a regular on ABC, CBS, Fox, CNBC, CNN, Yahoo, The View, and PBS. He has also been profiled in many major publications, including the New York Times, BusinessWeek, USA Today, People, Reader’s Digest, Time, Financial Times, Washington Post, Wall Street Journal, Working Woman, Glamour, Family Circle, Redbook, Huffington Post, Business Insider, Investors’ Business Daily, and Forbes.

Housing Affordability in California: The Breakdown

Ability to purchase a median-priced home: According to the State Legislature in Q1 of 2019 only 28% of the population in Napa County can afford to purchase a median-priced home compared to Lassen county with 63% (the highest affordable county). A couple of others: San Francisco and Santa Cruz - 20%, Santa Clara - 23%, San Diego - 26% and LA and Mendocino - 27%. For any other counties of interest please contact me.

1 out of 4 homeless people live in California. The states with the largest increases from 2016-2017 are:

California - 16,136 (13.7%)

New York - 3,151 (3.6%)

Oregon - 715 (5.4%)

Nevada - 435 (5.9%)

Texas - 426 (1.8%)

The Minimum Annual Income Required During Affordability Peak (Q4 2012) vs. Current.

Region 2012 Q1 2019 Q1 %CHG

CA Single Family Housing $ 56,320 $ 114,860 103.9%

CA Condo/Townhomes $ 44,440 $ 94,690 113.1%

Los Angeles Metro Area $ 53,780 $ 107,110 99.2%

Inland Empire $ 35,170 $ 76,810 118.4%

S.F. Bay Area $ 90,370 $ 186,230 106.1%

US $ 32,000 $ 53,620 67.6%

Existing Home Sales Point Toward a Good Time to Sell

Some Highlights:

Existing Home Sales dropped 1.7% from May to a seasonally adjusted annual rate of 5.27 million in June.

Low inventory levels are still a factor in the market. The current supply of homes for sale is at 4.4 months, which is less than the optimal 6-month supply.

Median home prices were up 4.3% from June 2018, hitting $285,700. This marked the 88th consecutive month with year-over-year price gains.

How to Increase Your Equity Over the Next 5 Years

Many of the questions currently surrounding the real estate industry focus on home prices and where they are heading. The most recent Home Price Expectation Survey (HPES) helps target these projected answers.

Here are the results from the Q2 2019 Survey:

Home values will appreciate by 4.1% in 2019

The average annual appreciation will be 3.2% over the next 5 years

The cumulative appreciation will be 16.8% by 2023

Even experts representing the most “bearish” quartile of the survey project a cumulative appreciation of over 6.7% by 2023

What does this mean for you?

A substantial portion of family wealth comes from home equity. As the value of a family’s home (an asset) increases, so does their equity.

Using the projections from the HPES, here is a look at the potential equity a family could earn over the next five years if they purchased a $250,000 home in January of 2019:

Based on gains in home equity, their family wealth could increase by $42,000 over that five-year period.

Bottom Line

If you don’t yet own a home, now may be the time to purchase. Owning or moving up to your dream home could allow you to ride the increase in equity of a growing asset.

Now's the Time To Move-Up and Upgrade Your Current Home

Homes priced at the top 25% of the price range for a particular area of the country are considered "premium homes." In today’s real estate market, there are deals to be had at the higher end! This is great news for homeowners wanting to upgrade from their current house.

Much of the demand for housing over the past couple of years has come from first-time buyers looking for their starter home. Many of the more expensive homes listed for sale have not seen as much interest.

According to ILHM’s Luxury Report, this mismatch in demand and inventory of luxury and premium homes has created a Buyer’s Market. For the purpose of the report, a luxury home was defined as one that costs $1 million or more.

“A Buyer’s Market indicates that buyers have greater control over the price point. This market type is demonstrated by a substantial number of homes on the market and few sales, suggesting demand for residential properties is slow for that market and/or price point.”

The authors of the report were quick to point out that current conditions at the higher end of the market are no cause for concern.

“While luxury homes may take longer to sell than in previous years, the slower pace, increased inventory levels and larger differences between list and sold prices, represent a normalization of the market, not a downturn.”

Luxury can mean different things to different people. To one person, luxury is a secluded home with plenty of property and privacy. To another, it could be a penthouse at the center of a bustling city. Knowing what characteristics mean luxury to you will help your agent find you the home of your dreams.

Bottom Line

If you are debating upgrading your current house to a premium or luxury home, now is the time!

New Apartments in Napa

Rents at emerging 282-unit complex start at $2,384. These apartments are just north of another housing project, 49-unit Stoddard West apartments for low-income families sponsored by the Gasser Foundation. Read the full article here or below:

The leasing center for The Braydon, Napa’s new, amenity-rich apartment complex, opened just more than a week ago, and the first residents have already signed leases, moved in and are calling the complex west of Soscol Avenue’s Auto Row home.

Residents can choose from one-, two- or three-bedroom units from 752 to 1,311 square feet. Lease rates for one bedroom, one bath unit start at $2,384 per month, two bedroom leases start at $2,810, and the three bedroom leases start at $3,253.

According to Zumper, a rental website, the average market-rate rent for a two-bedroom apartment in Napa during May was $2,240.

About 20 of the 282 planned units are done, said Easther Liu, national vice president of marketing for Fairfield Residential.

Fairfield Residential is developing the 7.37-acre housing site, which uses a new mailing address of 791 Vista Tulocay Lane. It is located on the west side of Soscol Avenue, just north of Tulocay Creek, with views of the Napa River.

A website for The Braydon shows photos of the sample apartments and the complex, which will also include a co-working space, gated dog park, pool, courtyard with outdoor dining space and cabanas, fitness center and “social lounge with full kitchen and multiple seating nooks.”

Once completed, a total of nine buildings will contain the almost 300 apartment homes at The Braydon. A leasing center, located next to a roundabout at the middle of the complex, is now open and staffed.

Inside the complex, the size and scope of the project — one of Napa’s largest apartment developments — is apparent. Chain link fencing wraps around the extensive construction project, which stretches both north and south of the leasing center and the first completed apartment building. The square footage of the apartment housing totals 278,256 square feet.

Napa’s Gasser Foundation originally launched the development, which was formerly known as Vista Tulocay Apartments.

The Gasser Foundation agreed to sell the then-Vista Tulocay site to BLT Enterprises for $9 million in 2002, but the sale did not close until 2013 because of flood control and entitlement delays.

Fairfield Residential bought the project from BLT Enterprises in February 2017 for an estimated $34.25 million.

The apartments are just north of another housing project, the 49-unit Stoddard West apartments for low-income families sponsored by the Gasser Foundation.

Stoddard West previously announced rents will be in the $475-to-$1,300 per month range, depending on the tenants and the number of rooms in the apartment.

Stoddard West, a partnership between Gasser and Burbank Housing of Sonoma County, closed its application list after receiving more than 500 applicants.

Liu declined to provide the number of applications Fairfield has received for the Braydon units.

The "Fastest Growing Trend" in the Housing Industry

Speaking of Rentals…Don’t forget about the rental on the Silverado Trail between Pratt Ave and Deer Park Rd. A private residence with 2 bedrooms with en-suite full bathrooms, open concept 1,728 sq ft home, 200 sq ft private deck with sweeping views of the valley and vineyards, less than 5 min from downtown St. Helena, walking distance to Meadowood. Message me if you know of anyone interested. Click here for more information.

An article from CBS indicates that builders are now investing in homes to then update them and rent them out as rentals seem to be on the rise. Take a look further at the atricle here or below.

KEY POINTS

Demand for single-family rental homes is surging, and homebuilders are now stepping in, redesigning and re-imagining the sector — and becoming landlords themselves.

“We basically took an apartment and went horizontal instead of vertical,” says Mark Wolf, founder and CEO of AHV Communities.

“Our business is booming right now with build-to-rent feasibility work,” says consultant John Burns.

Demand for single-family rental homes is surging, and homebuilders are now stepping in, redesigning and reimagining the sector — and becoming landlords themselves.

While builders have always sold some of their new homes to investors as rentals, the strong demand has some moving into the space exclusively.

AHV Communities, partnering with Bristol Group, is putting up 250 new detached homes in fast-growing San Antonio. Pradera is a gated community with three- and four-bedroom homes, renting from about $1,800 to $2,300 per month. The community includes luxury amenities, like a pool, fitness center, community kitchen and party space, as well as a dog park and dog-washing station.

“We basically took an apartment and went horizontal instead of vertical,” AHV founder and CEO Mark Wolf said. “About 93% of the apartment stock consists of studios, one and two bedrooms, very few three bedrooms. We saw a growing need coming out of the downturn, to provide three- and four-bedroom homes to the renter society.”

Wolf, who has experience in the multifamily apartment market, saw a need for more single-family homes after the housing crash, and he says that demand has not fallen off. While the homeownership rate has risen from its historic low in 2016, it is now starting to slip again.

“We think there’s a major shift in the demographics. Empty nesters are done taking care of their homes. They want to downsize, they want portability, mobility in the lease. The millennial household formation, they’re not really dialed into taking care of a home, they want to go out and do the same thing that the boomers are doing, which is enjoy life, not work hard for their house,” said Wolf.

Last year, about 43,000 single-family homes were built for rent, the largest number in nearly 40 years according to National Association of Home Builders analysis of U.S. Census data. The built-for-rent share of housing starts is also rising, nearly double its recent historical average (from 1992-2012).

Millennials Taylor Walters and Paree Dilkes want to get out of their rental apartment and into a larger single-family home.

“So we’ve been looking online for months now, whether to buy or whether to rent, and this is definitely up our alley,” Walters said as the two toured the amenities at Pradera. They are not married and have no children, but they do have a big dog.

“That’s really the biggest thing. It’s very inconvenient to have to take him out every time he needs to go. Having a yard would be awesome, just let him out, and also a little bit more space. We have a pretty good-sized apartment right now, but just kind of the feeling of being in a house,” said Dilkes.

Renting used to come with a social stigma, since homeownership was touted as the American Dream. The average annual household income of tenants in Pradera, however, is over $100,000, meaning many of them can afford to buy a home but simply choose not to.

Walters and Dilkes considered buying, but didn’t like the way the math worked out.

“I’ve done research, read different articles on millennials buying houses, and I think the biggest thing is the hidden costs that we might incur,” said Walters.

Stephanie Dixon and her husband recently sold their San Antonio home and moved into the rental community. Their children are in college or graduated, and they wanted an easier lifestyle.

“If the water heater breaks, you know, I don’t have to replace it. I just call them. I mean, even the air filters, they came and changed my air filters yesterday. I don’t have to worry about all that, that’s extra expense,” said Dixon.

Builders are struggling right now to put up the entry-level homes that are most in demand. The high costs of land, labor, materials and regulation make low-priced homes more difficult to profit from. That partly explains the shift toward rental properties and communities.

“Our business is booming right now with build-to-rent feasibility work,” said John Burns, founder and CEO of John Burns Real Estate Consulting. “We are discussing new projects with clients almost daily. The market has become so hot that we are already having conversations about when we will conclude the market is overbuilt.”

Burns says equity money is flowing in fast, and learning quickly that they need to partner with an experienced builder. That is why homebuilders Lennar and Toll Brothers have recently started building homes specifically to sell to investors as rentals.

“Most publicly traded builders are talking about building it for others rather than taking the risk themselves, while private builders are looking at taking more risk,” Burns said.

Wolf sees the build-for-rent market as less risky, especially in the short term.

“We believe in the long-term cash flow game. So if you hold these properties for 10-plus years, or even seven-plus years, the residual cash flow is worth more than the sale one time,” said Wolf.

AHV is building another rent-only community, in New Braunfels, Texas, in partnership with American Homes 4 Rent, a single-family rental REIT. The single-family REIT space grew out of the foreclosure crisis and has now consolidated to a few big players. They own several thousand homes, but they are spread out across communities, so management is more complicated and more expensive.

“They see the, I think, the benefit and the beauty of this model to complement what they already have,” said Wolf.

Home Prices Up 5.05% Across the Country

Some Highlights:

The Federal Housing Finance Agency (FHFA) recently released their latest Quarterly Home Price Index report.

In the report, home prices are compared both regionally and by state.

Based on the latest numbers, if you plan on relocating to another state, waiting to move may end up costing you more!

8 Real Estate Investing Mistakes to Avoid

With the stock market volatility real estate investing is becoming more popular. Here are 8 mistakes to avoid in order to make your real estate portfolio successful.

Buying Without Researching: Rushing into real estate without understanding what you’re getting can lead to bad results, says Kyle Whipple, a financial advisor and registered investment at advisor at C. Curtis Financial Group in Plymouth, Michigan. “Just because real estate is doing well doesn’t mean it will turn out to be a good investment for you.” Stock investors are often told to “buy low, sell high” and that same rule can be put to use for property investments. “You want to make sure that you’re getting a good deal and not purchasing an overpriced piece of real estate which will lower your long-term returns,” Whipple says.

Developing a Tunnel Vision: Real estate adds a new dimension to a portfolio, in terms of balancing against the risk and volatility associated with stocks. Kaufman says a common mistake is being too narrow about property focus. “Many individuals fail to diversify their real estate holdings,” he says, investing only in one local geographic area or property type. “This all-eggs-in-one-basket approach drastically increases downside risk, but investors do this because they are more comfortable investing in markets they’re familiar with.” Casting the net wider to incorporate crowdfunded investments or real estate investment trusts, known as REITs, can offer exposure to a broader group of properties and increase diversification.

Going It Alone: Owning a commercial or residential rental property can be both time- and capital-intensive. Trying to handle it all solo can require a level of focus and commitment that may not be realistic for every investor. A simple way to avoid that mistake is building a team from day one, says Kevin Ortner, president and CEO of Renters Warehouse in Minneapolis. That may involve investing with a partner or working with a broader group of individuals that includes an experienced real estate agent, an attorney who’s well-versed in property law, professional contractors and a property management company. Having support can make investing in real estate a smoother experience, with less room for error.

Relying on Bad Advice: When seeking out help in making decisions regarding property investments it’s important to go to the right sources. “Making an investment in real estate, especially for first-time investors, can be daunting and nerve-wracking,” says Rowena Dasgupta, an agent at Warburg Realty in New York. “Often, people ask friends and family for their opinion more for reassurance than for legitimate guidance.” What they should be doing instead, Dasgupta says, is seeking counsel from real estate professionals or an investor with a lengthy track record of buying and selling properties. These individuals have the knowledge and experience to provide more reliable advice.

Assuming It’s Easy: Just like stocks, mutual funds, bonds or other investments, real estate requires a certain amount of know-how to navigate. Terrell Gates, founder and CEO of Virtus Real Estate Capital, says both large and small real estate investors can make the mistake of thinking that investing in property is easier than it is. This can be exacerbated in bull markets when real estate is going strong because people tend to forget about previous downturns. “Unfortunately, to be consistently successful in real estate over the long haul requires more skill than luck,” Gates says.

Chasing Bargains: Ortner says another common pitfall among real estate investors is only looking for a deal when buying a property. “If you’re going to make long-term real estate investments, you don’t need to buy at a major discount,” Ortner says. “You just need to do deals that make sense, because, over time, you’re going to be building equity.” He says many investors limit the properties they can buy because they’re hoping to land a major discount with value, which isn’t a realistic target in the current market environment. By maintaining a long-term outlook, investors can avoid the bargain hunter mentality and focus instead on growing their property portfolio.

Not Having an Exit Strategy: Real estate can be a good buy-and-hold option but failing to develop an exit strategy can be damaging. Whipple has seen this scenario play out firsthand, with investors selling a highly appreciated piece of property without a plan in place for what to do with the funds. “They feel they are done with the real estate game and want out,” he says. “Unfortunately, they end up getting hit with a lot of taxes.” Having an end-play for real estate investments from day one can help avoid costly situations when it’s time to sell.

Overlooking the Bigger Picture: The worst mistake with real estate investing may simply be not considering how to utilize it within a broader portfolio. “Many investors make mistakes when they don’t understand how real estate fits into their overall strategy that includes diversification, long-term appreciation, liquidity needs and cash flow,” says Brent Weiss, co-founder and chief evangelist of Facet Wealth. Having a financial plan that incorporates real estate begins with understanding investment goals, risk tolerance and time horizon. These are things a financial advisor can help with. “Once investors understand what strategy will support their plan, they can determine the right mix of asset classes to create success,” Weiss says.

Article from USNews

The Cost of Waiting: Interest Rates Edition

Some Highlights:

Interest rates are projected to increase steadily heading into 2020.

The higher your interest rate, the more money you will end up paying for your home and the higher your monthly payment will be.

Rates are still low right now – don’t wait until they hit 5% to start searching for your dream home!